Testimony, Comments, Correspondence

Reducing Regulatory Barriers in Federal Housing Programs: Summary of NCSHA’s Recommendations

In response to the White House Council on Eliminating Regulatory Barriers to Affordable Housing and on behalf of its member state housing finance agencies, on January 31, 2020, NCSHA recommended specific steps the Departments of Agriculture, Housing and Urban Development, and Treasury can take that will lead directly to more affordable housing financing and development. This chart offers a summary of those recommendations.

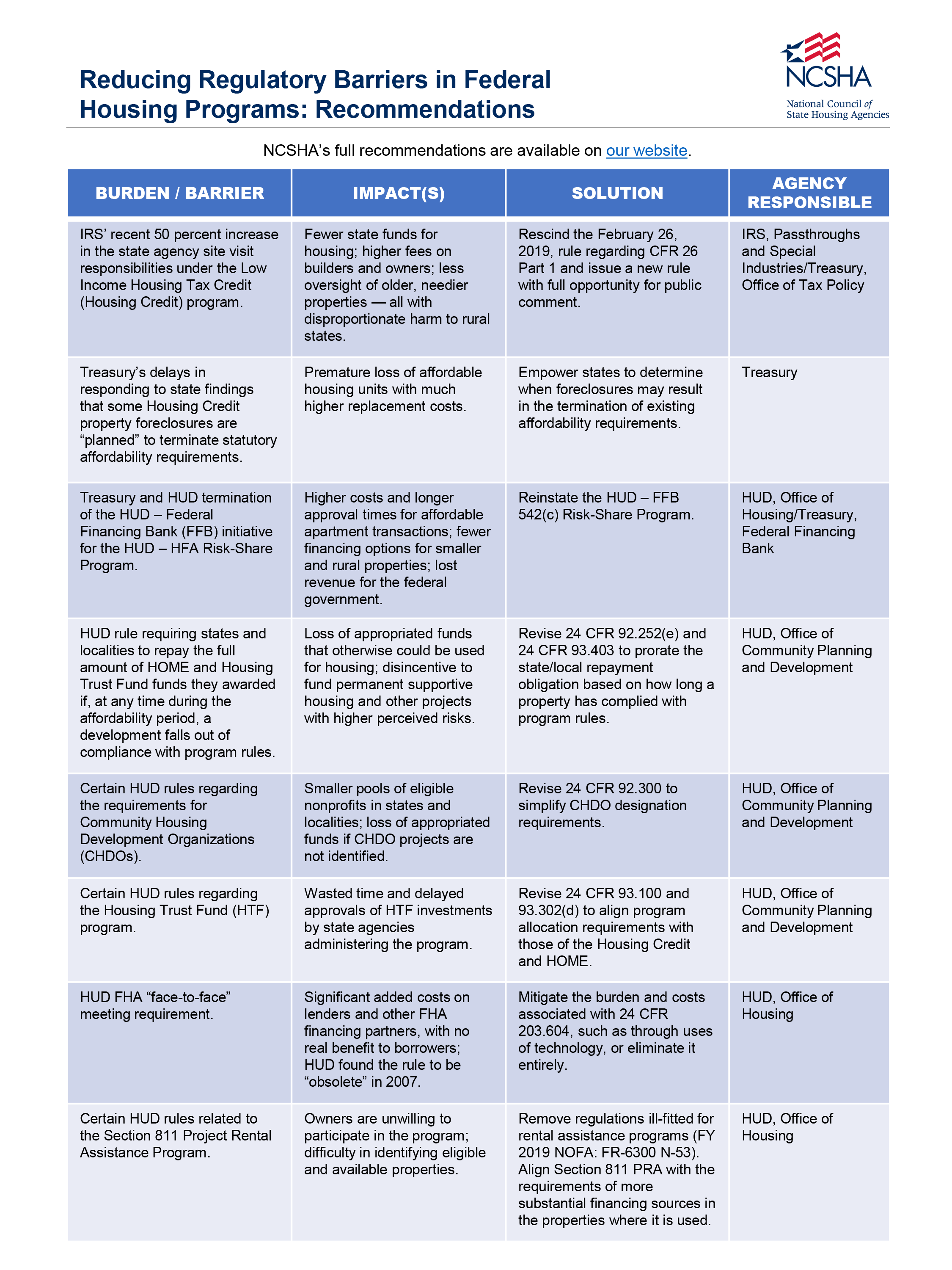

Reducing Regulatory Barriers in Federal Housing Programs: NCSHA’s Recommendations

In response to the White House Council on Eliminating Regulatory Barriers to Affordable Housing and on behalf of its member state housing finance agencies, on January 31, 2020, NCSHA recommended specific steps the Departments of Agriculture, Housing and Urban Development, and Treasury can take that will lead directly to more affordable housing financing and development.

ACTION Statement on Infrastructure and the Housing Credit

The A Call To Invest in Our Neighborhoods (ACTION) Campaign, which NCSHA co-chairs, provided this statement to members of the House Ways and Means Committee in response to its January 27, 2020, hearing, “Paving the Way for Funding and Financing Infrastructure Investments.”

NCSHA Comments to FHFA on GSE Pooling Practices

This document is NCSHA's comment letter to FHFA raising HFAs' concerns to Director Calabria about the RFI on the GSEs' UMBS pooling practices. This letter was sent to FHFA on January 21, 2020.

Industry Comments to FHFA on GSE Pooling Practices

This document is a joint letter from housing industry organizations to FHFA on its RFI regarding GSE UMBS pooling practices. It was sent to FHFA Director Mark Calabria on January 17,...

Salazar Testimony Before the House Financial Services Subcommittee on Housing, Community Development, and Insurance

Oregon Housing and Community Services Executive Director and NCSHA Secretary/Treasurer Margaret Salazar represented the nation’s state housing finance agencies on November 20 during a hearing before the House Financial Services Subcommittee on Housing, Community Development, and Insurance focused on the health, safety, and soundness of HUD-assisted rental and public housing.

NCSHA Comments on IRS Notice 2019-52

The National Council of State Housing Agencies (NCSHA) appreciates the opportunity to provide our perspectives on the Internal Revenue Service (IRS) request for comments in Notice 2019-52 regarding possible improvements to Revenue Procedures 2014-49 and 2014-50 regarding natural disasters.

NCSHA Comments on CFPB ANPR on Qualified Mortgage Definition Under the Truth in Lending Act

On September 16, 2019, NCSHA submitted comments to the Director of the Consumer Financial Protection Bureau, Kathy Kraninger, on the Bureau's Advance Notice of Proposed Rulemaking on the Qualified Mortgage Definition under the Truth in Lending Act.

QM Coalition Letter to CFPB on Qualified Mortgage Definition DTI Limit

This letter, signed by 23 industry stakeholders, was sent to CFPB Director Kathy Kraninger in response to the Advance Notice of Proposed Rulemaking on the Qualified Mortgage Definition under the Truth in Lending Act (Regulation Z).