HUD Report Shows Continued Success of Single Family Loan Sale Program

Earlier this week, HUD released its most recent Report to the Commissioner on Post-Sale Reporting on the FHA Single Family Loan Sale (SFLS) program. The report, using data through August 3, 2015, found that the SFLS program continues to meet its intended goals of contributing to the Mutual Mortgage Insurance (MMI) fund, providing homeowners who have exhausted FHA’s loss mitigation options a second chance to stay in their homes, and reducing taxpayer risk.

Instituted in 2010, the SFLS program is intended to maximize financial recovery, reduce claim costs, minimize the time assets are held, and keep homeowners in their homes. The SFLS program enables FHA to accept assignment of FHA-insured loans and sell distressed mortgages prior to foreclosure, avoiding costly and potentially lengthy foreclosure proceedings. When a distressed loan is sold, FHA generates savings by avoiding claim, holding, and sales expenses that would have occurred if the loan was foreclosed upon.

The report states that FHA has sold roughly 101,000 distressed mortgage notes through the Distressed Asset Stabilization Program (DASP), with roughly 55 percent of those sold mortgage notes now resolved. Nearly 50 percent of the loans that have come to a resolution have successfully avoided foreclosure. The report found that without DASP, the alternative for these homeowners would have most likely been foreclosure and the loss of their home.

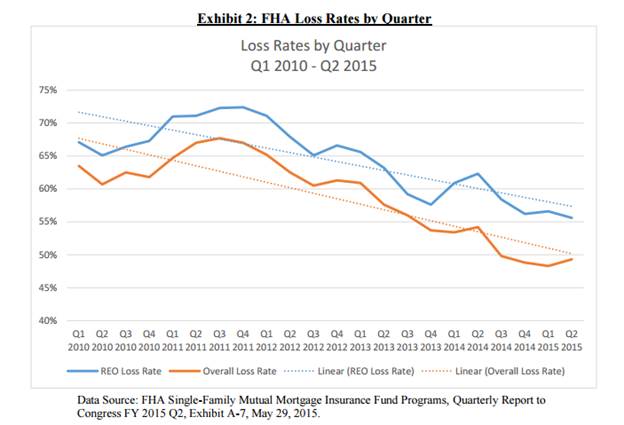

HUD found that the 14 rounds of SFLS mortgage sales since 2010 have increasingly improved the financial health of the MMI fund. Overall, loss rates to the MMI fund have dropped from 64 percent in the first quarter of 2010 to 49 percent in the second quarter of 2015.

FHA says in the report that it is continuously looking to build on the success of the SLFS program and improve its contributions to the MMI fund as well as provide more homeowners different avenues to avoid foreclosure. In the report, FHA details the following changes that were made to the SLFS program in 2015:

- Required loan purchasers not to foreclose on borrowers for 12 months in owner-occupied properties;

- Required loan purchasers to evaluate the borrower for the Home Affordable Modification Program (HAMP). The purchaser is required to offer HAMP or a substantially similar modification to eligible borrowers;

- Created a pool of loans where only nonprofit groups and local governments were eligible to participate in the auction; and

- Conducted outreach to encourage a greater number of nonprofits to participate in the SFLS program.