State Housing Finance Agencies: At the Center of the Affordable Housing System

High housing costs have become a painful reality for millions of Americans in recent years, imposing difficult financial hardships and fueling persistent inflation.

The challenges facing lower-income renters, aspiring first-time home buyers, and cash-strapped owners of older homes are different — but they all reflect the same underlying fact: Almost anywhere you look, America has a housing affordability crisis.

State housing finance agencies are at the center of the solutions.

HFAs have delivered more than $800 billion in financing to make possible the purchase, development, and rehabilitation of more than 8.2 million affordable homes

and rental apartments for low- and middle-income households.

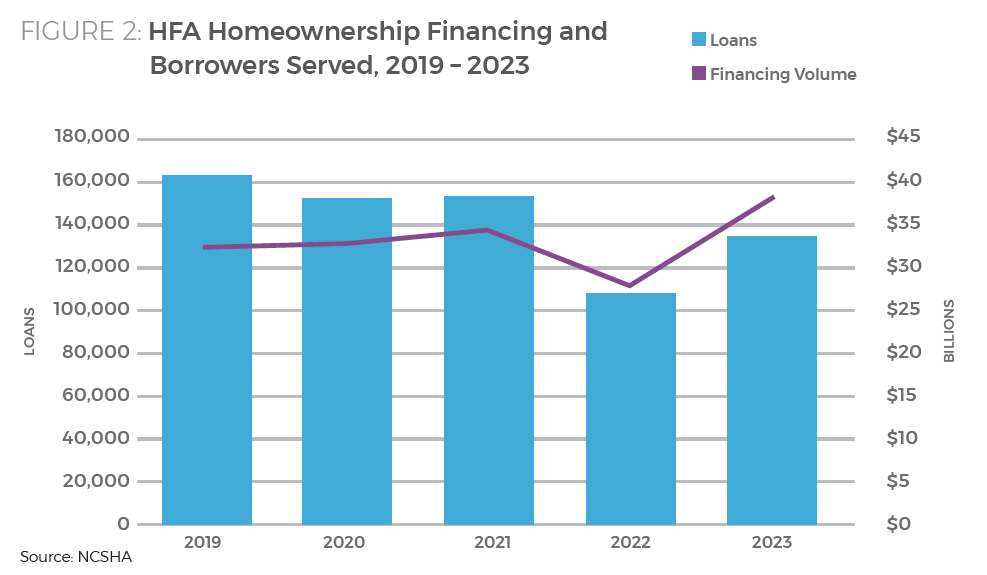

Every year, these agencies help 250,000 – 275,000 owners and renters all across the country.

HFAs combine the financial tools and business discipline of a large-scale lending institution with the planning and policy-making responsibilities of a mission-oriented, public-purpose agency. They are self-supporting — not reliant on taxpayers to operate.

Each HFA was created by its state to meet its own specific housing needs, so no two are exactly alike. They all share a common mission: to make housing affordable for those hit hardest by high housing costs.

This report describes how they do it.

AFFORDABLE HOMEOWNERSHIP

The Challenges

Homeownership, the primary driver of household wealth and a foundation for family stability, is increasingly out of reach for millions of Americans.

Home prices have increased more than 50 percent since 2019i and doubled over the past decade.ii Roughly 75 percent of homes on the market at the end of last year were unattainable for the middle class.iii The share of newly built homes serving entry-level buyers is less than 10 percent.iv And lower-income homeowners earning $55,000 or less have cumulative home repair needs of $57 billion.v

HFA Solutions

State HFAs have made homeownership more affordable for 4.4 million lower-income homeowners and home buyers. They do it by:

- financing affordable mortgages,

- providing down payment assistance,

- supporting affordable home construction, and

- funding necessary home improvements.

The Results

The Impacts

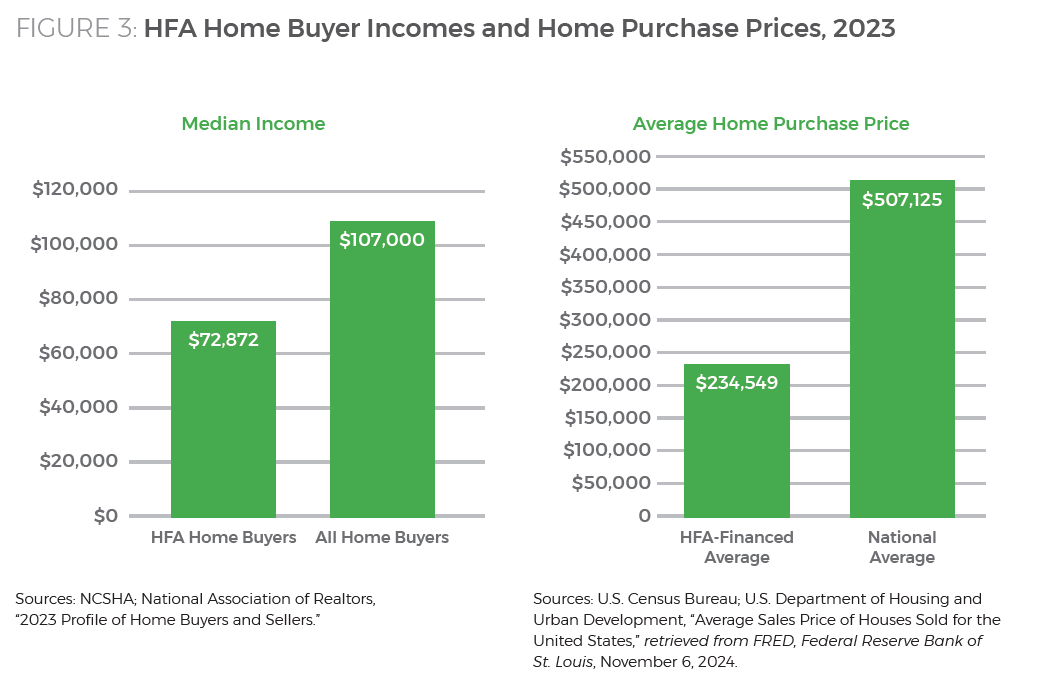

The median income of an HFA-financed home buyer is less than $75,000 — more than 30 percent below the national median for all home buyers. Their average home price is $235,000 — less than half of the national average. Nine in 10 HFA-supported owners are first-time home buyers.

AFFORDABLE RENTAL HOUSING

The Challenges

Record numbers of Americans are paying unsustainable rents, living in poor-quality apartments, and experiencing homelessness.

The average rent has increased 30 percent since 2019 — 50 percent more than average wages.vi Twelve million renters pay more than half their income for rent, while four million live in substandard conditions.vii Three out of every four households income-eligible for rental assistance don’t receive any.viii The supply of affordable apartments is millions short of demand,ix and low-cost rentals are being lost faster than new ones can be built.x

HFA Solutions

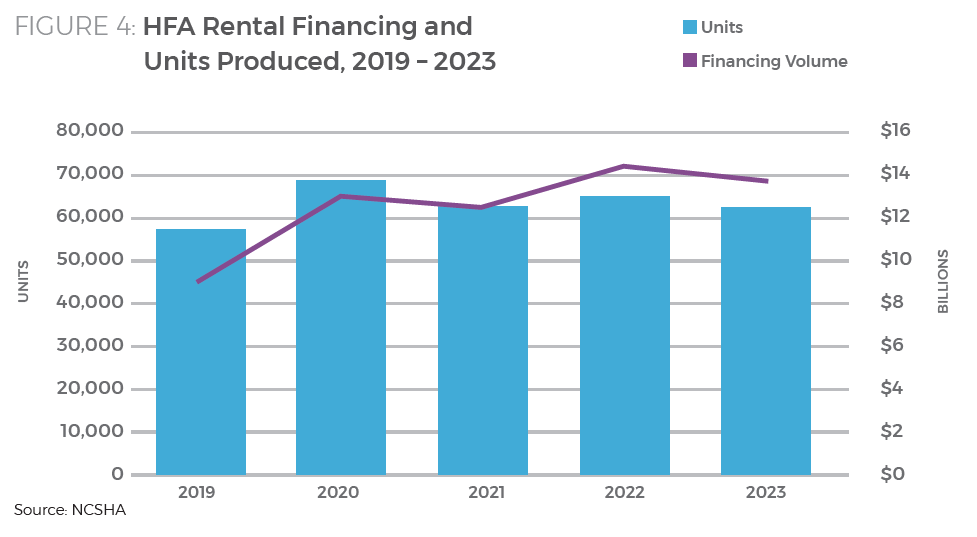

State HFAs have provided lower-cost homes and improved housing conditions by financing more than 3.8 million apartments for low-income renters. They do it by:

- financing apartment development,

- allocating construction incentives,

- delivering rental assistance, and

- ensuring quality property standards and timely rent collection.

The Results

The Impacts

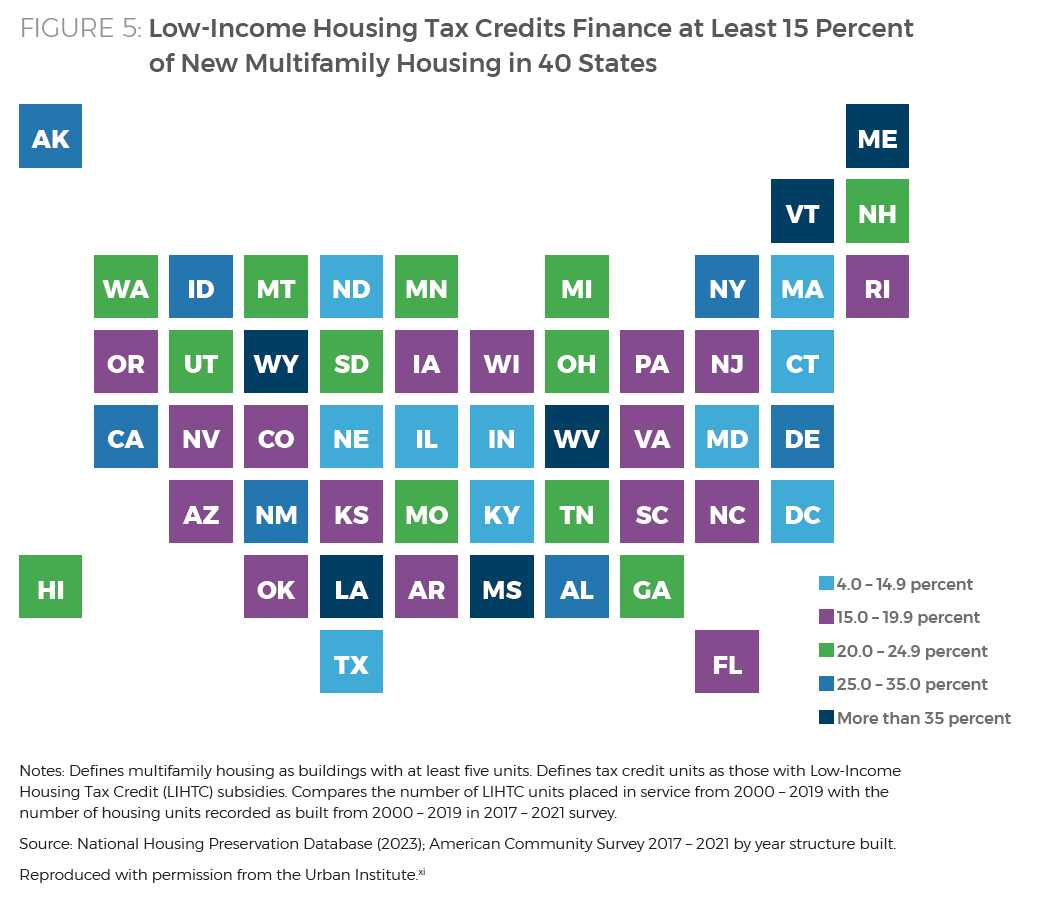

Eighty-five percent of HFA-financed apartments serve households earning 60 percent of their area’s median income or less. The main HFA-administered rental assistance program supports renters with an average income of $13,500. The federal Low-Income Housing Tax Credit (LIHTC) program, administered in 53 states and territories by the HFA, serves mostly extremely low-income people and drives apartment development across the country.

THE FOUNDATIONS OF HFA EFFECTIVENESS

Strong Management

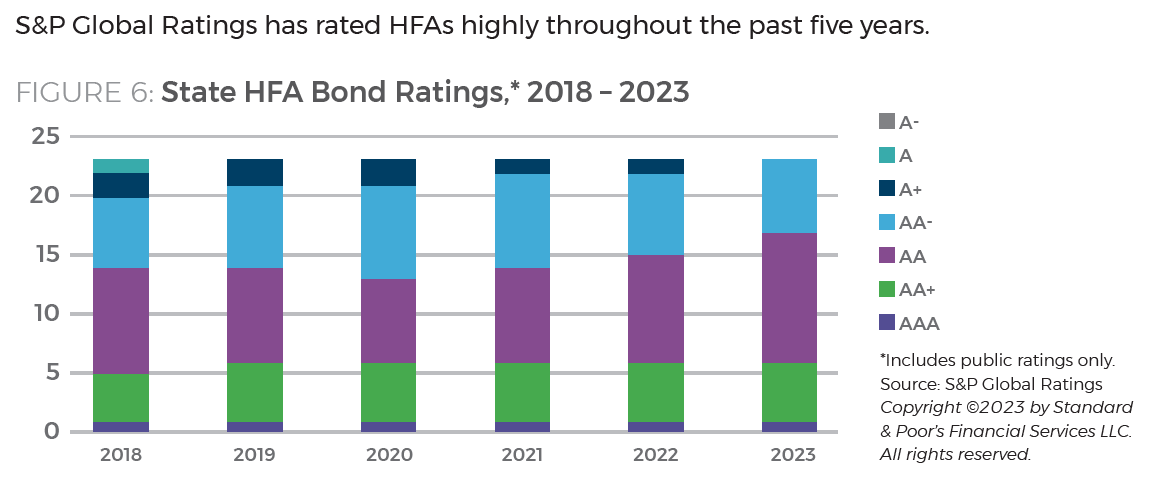

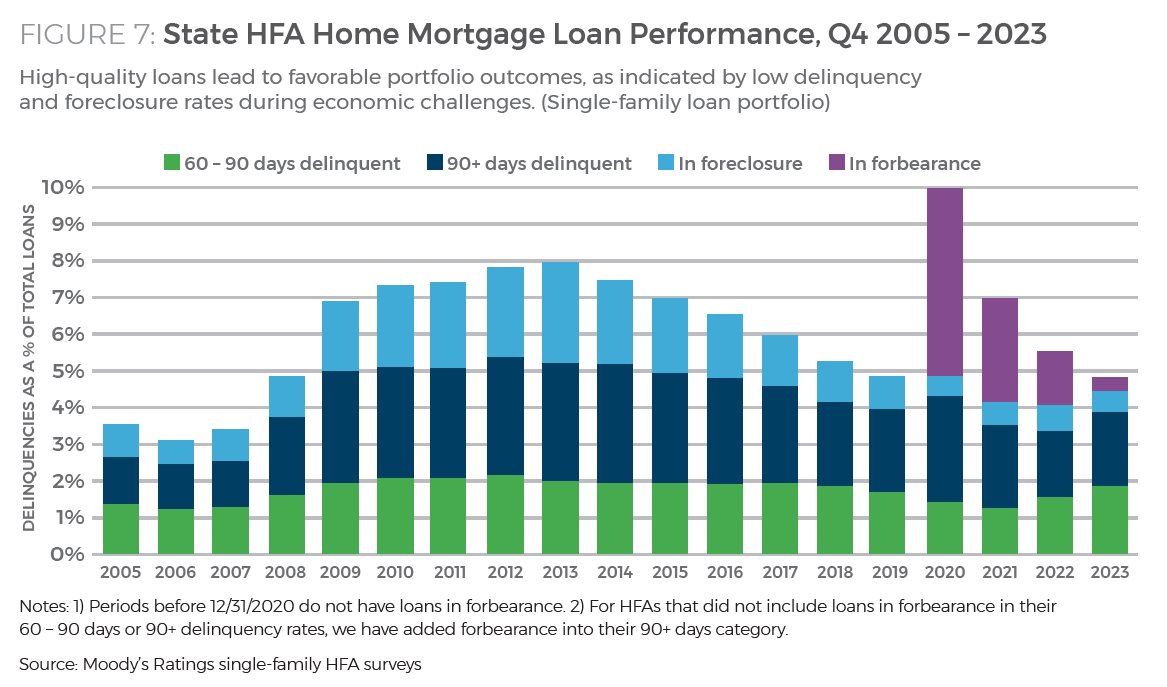

Superior Financial Performance

Analysis by Moody’s Ratings attests to HFA loan quality.

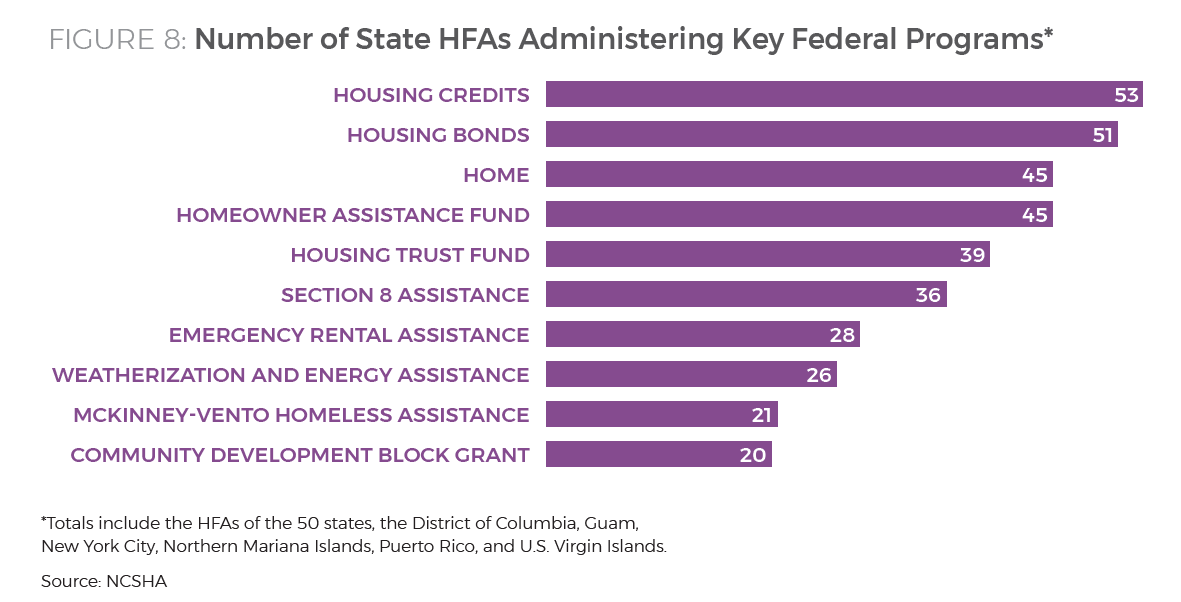

Sound Stewardship of Federal Resources

HFAs are the primary administrators of most major federal housing programs, reflecting a long-running, bipartisan confidence that they are best positioned to serve both national housing objectives and specific state needs. Governors and state legislatures in every part of the country are also turning to state HFAs to solve their housing challenges as never before.

State HFAs

- Alabama Housing Finance Authority

- Alaska Housing Finance Corporation

- Arizona Department of Housing

- Arkansas Development Finance Authority

- California Housing Finance Agency

- Colorado Housing and Finance Authority

- Connecticut Housing Finance Authority

- Delaware State Housing Authority

- District of Columbia Housing Finance Agency

- Florida Housing Finance Corporation

- Georgia Department of Community Affairs/Georgia Housing and Finance Authority

- Hawaiʻi Housing Finance and Development Corporation

- Idaho Housing and Finance Association

- Illinois Housing Development Authority

- Indiana Housing and Community Development Authority

- Iowa Finance Authority

- Kansas Housing Resources Corporation

- Kentucky Housing Corporation

- Louisiana Housing Corporation

- MaineHousing

- Maryland Department of Housing and Community Development

- MassHousing

- Michigan State Housing Development Authority

- Minnesota Housing

- Mississippi Home Corporation

- Missouri Housing Development Commission

- Montana Housing

- Nebraska Investment Finance Authority

- Nevada Housing Division

- New Hampshire Housing Finance Authority

- New Jersey Housing and Mortgage Finance Agency

- New Mexico Mortgage Finance Authority

- New York City Housing Development Corporation

- New York State Homes and Community Renewal

- North Carolina Housing Finance Agency

- North Dakota Housing Finance Agency

- Ohio Housing Finance Agency

- Oklahoma Housing Finance Agency

- Oregon Housing and Community Services

- Pennsylvania Housing Finance Agency

- Puerto Rico Housing Finance Authority

- Rhode Island Housing

- South Carolina State Housing Finance and Development Authority

- South Dakota Housing Development Authority

- Tennessee Housing Development Agency

- Texas Department of Housing and Community Affairs

- Utah Housing Corporation

- Vermont Housing Finance Agency

- Virgin Islands Housing Finance Authority

- Virginia Housing

- Washington State Housing Finance Commission

- West Virginia Housing Development Fund

- Wisconsin Housing and Economic Development Authority

- Wyoming Community Development Authority

![]()

Sources

i Schaul, Kevin and Lerman, Rachel. “Are home prices still rising? See how prices have changed in your area.” The Washington Post, May 14, 2024, www.washingtonpost.com/business/interactive/2024/housing-market-price-trends-zip-code-map/.

ii Jones, Jonathan. “Cities with the Largest Increase in Home Prices Over the Last Decade.” www.constructioncoverage.com, June 29, 2024, https://constructioncoverage.com/research/cities-with-the-largest-home-price-growth-last-decade.

iii National Association of Realtors. “U.S. Housing Market Needs More Than 300,000 Affordable Homes for Middle-Income Buyers.” www.nar.realtor, June 8, 2023, www.nar.realtor/newsroom/us-housing-market-needs-more-than-300000-affordable-homes-for-middle-income-buyers.

iv The White House. “Increasing the Supply of Affordable Housing: Economic Insights and Federal Policy Solutions.” www.whitehouse.gov, March 2024, https://www.whitehouse.gov/wp-content/uploads/2024/03/ERP-2024-CHAPTER-4.pdf.

v Divringi, Eileen. “Research Brief: Updated Estimates of Home Repair Needs and Costs.” Federal Reserve Bank Philadelphia, March 2023, www.philadelphiafed.org/-/media/frbp/assets/community-development/reports/23-02-home-repairs-update.pdf.

vi Lee, Kenny. “Rents Grow Faster Than Wages Across the US — and NYC Feels the Brunt.” StreetEasy Reads blog, May 7, 2024, https://streeteasy.com/blog/rents-grow-faster-than-wages-across-us-nyc/.

vii Airgood-Obrycki, Whitney and Wedeen, Sophia. “Six Takeaways from America’s Rental Housing 2024.” Joint Center for Housing Studies of Harvard University, Housing Perspectives blog, January 25, 2024, www.jchs.harvard.edu/blog/six-takeaways-americas-rental-housing-2024.

viii Brey, Jared. “If Congress Cuts Section 8 Housing, These States Will Suffer.” www.governing.com, March 20, 2023, www.governing.com/community/if-congress-cuts-section-8-housing-these-states-will-suffer.

ix Zumbrun, Josh. “How Severe Is the Housing Shortage? It Depends on How You Define ‘Shortage.’” The Wall Street Journal, April 14, 2023, www.wsj.com/articles/how-severe-is-the-housing-shortage-it-depends-on-how-you-define-shortage-89cdbee7.

x Joint Center for Housing Studies of Harvard University. “New Report Shows Rent Is Unaffordable for Half of Renters as Cost Burdens Surge to Record Levels.” www.jchs.harvard.edu, January 25, 2024, www.jchs.harvard.edu/press-releases/new-report-shows-rent-unaffordable-half-renters-cost-burdens-surge-record-levels.

xi Freemark, Yonah and Payton Scally, Corianne. “LIHTC Provides Much-Needed Affordable Housing, But Not Enough to Address Today’s Market Demands.” Urban Wire, July 11, 2023. www.urban.org/urban-wire/lihtc-provides-much-needed-affordable-housing-not-enough-address-todays-market-demands.[/one-half]